The share purchase agreement represents the most consequential document in any UAE acquisition. It allocates risk, defines obligations, establishes the purchase price mechanism, and ultimately determines who bears the cost when things go wrong. For private equity funds, corporate acquirers, and family offices executing UAE transactions, understanding how to draft and negotiate SPAs under UAE law is not optional.

Yet international standard forms—whether UK BVCA templates or US venture capital documentation—do not translate directly to the UAE context. Statutory pre-emption rights override contractual provisions. Notarization requirements create execution risks that sophisticated parties frequently underestimate. The relationship between the English-language SPA and Arabic constitutional documents introduces ambiguities that emerge only when enforcement becomes necessary.

This guide examines share purchase agreement drafting and negotiation specifically for UAE M&A transactions. It addresses the clauses that actually get litigated in UAE courts and arbitrations, the execution mechanics that cause deals to fail at the final stage, and the negotiation leverage points that separate experienced UAE practitioners from those applying international templates without adaptation.

Key Takeaways: UAE Share Purchase Agreements

Critical UAE-Specific Differentiators:

- Arabic notarized deed effects the transfer - The English SPA creates obligations, but the Arabic transfer agreement executed before a notary is what actually transfers shares under UAE law. Notarization = closing.

- Statutory pre-emption cannot be contracted around - Other LLC shareholders have 30-day statutory rights to acquire shares being sold to third parties. Structure transactions to address this.

- Competition clearance adds 90+ days - Mandatory pre-closing notification for deals meeting AED 300 million turnover or 40% market share thresholds (Cabinet Decision No. 3 of 2025). Suspensory regime.

- MOA takes precedence over private agreements - Rights granted in the SPA must be reflected in constitutional documents to bind the company and future shareholders.

- Post-corporate tax indemnities are critical - Tax warranties now require comprehensive coverage including QFZP status verification, with extended survival periods.

- Gratuity provisions are chronically understated - Independent calculation and specific indemnity essential; this is the most common hidden liability in UAE acquisitions.

- W&I insurance availability growing - Warranty and indemnity insurance now available from international insurers for UAE deals, typically 1-2% premium for 10-30% coverage.

- DIAC arbitration with DIFC seat is market standard - Combination provides common law approach, English proceedings, confidentiality, and international enforceability.

Why UAE SPAs Differ from International Standards

The fundamental error international acquirers make is treating UAE share purchases as jurisdictionally neutral transactions. They engage counsel familiar with private equity documentation generally but unfamiliar with UAE commercial law specifically, apply UK or US precedent agreements with minimal modification, and discover—often late in the transaction—that critical assumptions do not hold.

Statutory Pre-emption Rights Cannot Be Contracted Around

Under Federal Decree-Law No. 32 of 2021 on Commercial Companies, shareholders in UAE limited liability companies hold statutory pre-emption rights on share transfers to third parties. When an existing shareholder proposes to sell shares to a non-shareholder, other shareholders must be offered the opportunity to purchase those shares on the same terms. This right exists by operation of law and applies for a 30-day period from notification.

The commercial implication: your carefully negotiated exclusivity with the seller does not prevent other shareholders from exercising statutory rights to acquire the shares you have agreed to purchase. If multiple shareholders exercise pre-emption, allocation occurs pro-rata to existing shareholding percentages.

Private equity funds accustomed to exclusive negotiations with founders or controlling shareholders must account for this statutory overlay. The SPA should address pre-emption explicitly—requiring seller to obtain waivers from other shareholders, specifying what happens if pre-emption is exercised, and potentially structuring the transaction to minimize pre-emption exposure.

Constitutional Documents vs Private Agreements

In UAE onshore companies, registered constitutional documents—the Memorandum and Articles of Association—take precedence over private shareholder agreements in case of conflict. The MOA is filed with the Department of Economic Development, accessible to regulators and third parties, and constitutes the company's governing document.

The SPA, by contrast, is a private contract between buyer and seller. It binds those parties contractually but does not bind the company itself unless the company is a party to the agreement.

Where the SPA grants the buyer certain governance rights—board appointment, veto over specified matters, information rights—but the MOA does not reflect these provisions, the buyer may have a breach of contract claim against the seller personally while lacking enforceable rights against the company.

Sophisticated SPAs address this by including seller covenants to procure amendments to constitutional documents aligning the MOA with SPA provisions. However, amending the MOA requires shareholder approval, and minority shareholders not party to the SPA may refuse consent.

Structuring your acquisition correctly from the outset avoids these complications. Our corporate team advises on constitutional document alignment, shareholder consent strategies, and transaction structures that minimize execution risk. Contact us to discuss your UAE M&A transaction before signing.

Arabic Documentation and Notarization Create Execution Risk

UAE share transfers in onshore LLCs require execution of an Arabic-language share transfer agreement before a notary public, with subsequent registration at the DED. The process involves:

Document preparation: A short-form Arabic share transfer agreement summarizing key commercial terms must be prepared. This document is distinct from the long-form English SPA and must accurately reflect the agreed transaction.

Notary attendance: All parties—or their authorized representatives holding notarized powers of attorney—must appear before the notary. For foreign corporate buyers, this requires document legalization through UAE embassies, Ministry of Foreign Affairs attestation, and certified translation.

Immediate binding effect: Once the Arabic transfer agreement is executed at the notary, the transaction becomes binding under UAE law regardless of conditions in the English SPA that may not have been satisfied.

The risk: parties negotiate and sign a conditional English SPA (subject to regulatory approvals, third-party consents, or due diligence completion), then attend notarization assuming it is merely administrative. In fact, notarization creates immediate legal effect. If the transaction later fails to complete due to unsatisfied conditions, unwinding becomes complex.

We have seen transactions where buyers attended notarization believing it was preliminary, discovered conditions would not be satisfied, and faced expensive disputes over whether they were bound to complete despite condition failures.

Best practice: Ensure all conditions precedent are satisfied or waived before attending notarization. Treat notarization as closing, not signing.

Governing Law Does Not Solve All Problems

Many UAE SPAs specify English law or DIFC law as governing law, particularly where the buyer is a UK or international private equity fund. This choice is valid and generally respected by UAE courts and arbitrators.

However, governing law clauses have limits. UAE courts will apply mandatory provisions of UAE commercial law to UAE-incorporated companies regardless of the SPA's governing law. Statutory pre-emption rights, share capital maintenance rules, and director duties all derive from UAE law and cannot be contracted out of through governing law selection.

Additionally, enforcement ultimately occurs in UAE courts or UAE-seated arbitration. Even where English law governs the contract, the remedies available and procedural rules applicable will be those of the UAE legal system. Specific performance, interim relief, and damages calculations follow UAE or DIFC procedures, not English court practice.

Case Study: Notarization Timing Failure

A European private equity fund agreed to acquire a Dubai-based logistics company for AED 180 million. The English-law SPA was conditional on competition clearance under the new UAE competition regime. The parties signed the SPA and shortly thereafter attended the Dubai notary to execute the Arabic transfer agreement, which the buyer's counsel (unfamiliar with UAE practice) described as "administrative registration."

Competition clearance was subsequently denied. The buyer argued the transaction had not completed because the clearance condition was not satisfied. The seller argued that notarization effected the transfer regardless of the English SPA conditions, and demanded payment.

The dispute went to DIAC arbitration. The tribunal held that under UAE law, the Arabic transfer agreement executed before the notary created binding obligations, and the buyer could not rely on conditions in the English SPA to avoid completion once notarization occurred. The buyer was required to complete the purchase despite the competition authority's refusal.

The error was treating notarization as separate from closing rather than understanding that notarization constitutes closing under UAE law.

Anatomy of a UAE Share Purchase Agreement

A UAE share purchase agreement typically comprises three documentary layers, each serving distinct legal functions.

The Long-Form English SPA

The primary transaction document—typically 50 to 150 pages—is usually drafted in English and contains comprehensive terms:

- Parties and transaction structure

- Sale and purchase provisions (what shares, from whom, at what price)

- Consideration and payment mechanics

- Conditions precedent and seller undertakings

- Representations and warranties

- Limitations on claims (time limits, financial caps, disclosure)

- Indemnities and specific protections

- Restrictive covenants (non-compete, non-solicit, confidentiality)

- Post-completion obligations and dispute resolution

This document can specify English law, DIFC law, or UAE law as governing law. For cross-border transactions and institutional investors, English law or DIFC law is common due to familiarity and established precedent.

The English SPA is typically signed by parties in counterpart (electronic signature is generally acceptable) without notarization requirements. Signing creates contractual obligations between the parties but does not effect share transfer under UAE law.

The Arabic Short-Form Transfer Agreement

The second layer is a short-form Arabic transfer agreement—typically one to three pages—that must be executed before a UAE notary public. This document identifies:

- Transferor and transferee

- Target company and share details

- Number of shares and percentage being transferred

- Purchase price

- Confirmation that statutory pre-emption procedures were followed

This Arabic document is what actually effects the share transfer under UAE law. The notarization requirement serves both evidentiary and regulatory functions—it creates a formal record and facilitates subsequent DED registration.

English SPA vs Arabic Transfer Agreement: Key Differences

Critical point: The relationship between these documents is what catches international acquirers. The English SPA creates the contractual framework and obligations, but the Arabic transfer agreement executed at the notary is the moment shares actually transfer under UAE law. Parties must coordinate timing carefully—if you attend notarization before satisfying SPA conditions, you may be legally bound to complete regardless of those conditions.

Constitutional Document Amendments

The third layer involves amendments to the target company's Memorandum of Association to reflect the new ownership structure. These amendments require shareholder approval and must be filed with the DED.

If the SPA grants the buyer governance rights (board seats, veto rights, information access), corresponding amendments to the MOA should be included to ensure those rights bind the company itself and future shareholders.

Seller Representations and Warranties: What Actually Gets Litigated

Representations and warranties serve three functions in UAE M&A: risk allocation (who bears the cost if facts are inaccurate), disclosure forcing (requiring seller to reveal problems), and valuation adjustment (if breached, buyer recovers damages equal to the economic loss).

International SPA templates contain extensive schedules of representations addressing corporate status, financial condition, contracts, assets, intellectual property, litigation, environmental matters, and regulatory compliance. Most of these transfer readily to UAE transactions with modest adaptation.

However, certain representations require UAE-specific drafting, and understanding what actually generates warranty claims in UAE deals helps focus negotiation on material issues.

Trade License Validity and Permitted Activities

The target must hold a valid trade license from the relevant authority (DED for mainland entities, free zone authority for free zone companies). The license must authorize all activities the target actually conducts.

Standard warranty language:

"The Company holds a valid trade license issued by [authority] dated [date], license number [X], permitting the Company to conduct [listed activities]. The trade license is in full force and effect, not subject to any suspension or revocation proceedings, and all renewal fees have been paid."

Why this matters: Companies frequently expand into adjacent activities without updating licenses. A logistics company licensed for warehousing that provides customs brokerage services, or a trading company that begins manufacturing, creates regulatory exposure that transfers to the buyer in a share purchase. The DED can suspend licenses for unauthorized activity, and retrospective license amendments may not be available.

We see warranty claims on trade license scope more frequently than international acquirers expect. Buyers should verify license scope during due diligence and require specific warranties that all conducted activities fall within licensed activities.

Emiratisation Compliance

Since 2022, UAE companies meeting certain thresholds must employ specified percentages of UAE nationals. Non-compliance triggers monthly penalties and can affect license renewal.

UAE-specific warranty:

"The Company is in full compliance with all Emiratisation requirements applicable to it under applicable law and regulations, including [specify current percentage requirement]. The Company has employed [X] UAE nationals representing [Y]% of its workforce, has timely filed all required reports with the Ministry of Human Resources and Emiratisation, and has paid all required salaries to UAE national employees. No penalties, fines, or other sanctions have been imposed on the Company for Emiratisation non-compliance."

Negotiation point: Sellers often resist this warranty because Emiratisation requirements evolve rapidly and compliance obligations are not always clear. Buyers should establish the target's current Emiratisation position through due diligence and require disclosure of any pending MOHRE inquiries or historical non-compliance.

Wage Protection System Compliance

UAE labour law requires employers to pay salaries through the Wage Protection System, an electronic salary transfer system monitored by MOHRE. Non-compliance can result in work permit processing restrictions, fines, and in severe cases, criminal liability for management.

Key warranty elements:

"All employee salaries and benefits due and payable through [completion date] have been paid in full via the Wage Protection System. The Company has not received any notices, warnings, or inquiries from MOHRE regarding WPS non-compliance. No employees are owed unpaid wages, overtime, or other compensation."

What fails in practice: Sellers provide this warranty believing they are compliant, but due diligence reveals partial payments outside WPS (particularly for senior employees or incentive compensation), delayed salary transfers, or disputed overtime calculations that were never properly resolved.

These issues are expensive to remedy post-closing because back-pay obligations, penalties, and MOHRE proceedings can extend for years. Buyers should require specific indemnities for pre-closing WPS issues with longer survival periods than standard warranty claims.

End-of-Service Gratuity Provisioning

As discussed in our due diligence guide, gratuity liabilities are chronically under-provisioned in UAE companies. In share purchases, this liability transfers to the buyer automatically.

Specific warranty:

"The Company has adequately provisioned in its financial statements for all end-of-service gratuity obligations owed to employees calculated in accordance with UAE Labour Law. The Gratuity Schedule attached to this Agreement sets out the Company's calculation of accrued gratuity for each employee as of the Accounts Date, which calculation is accurate and complete. The total provisioned amount is sufficient to discharge all accrued gratuity obligations if all employees were terminated as of that date."

Buyer protection: Require the seller to calculate gratuity independently using current payroll data, and include this calculation as a disclosed schedule. Any shortfall between the disclosed calculation and the buyer's independent verification becomes a warranty breach. Consider requiring a specific indemnity for gratuity underprovision with the aggregate cap lifted for this specific risk.

Real Property Ownership and Encumbrances

For companies owning UAE real property, title verification is essential. Real property ownership in the UAE varies by emirate and area, with different registration systems and procedures.

Property warranty:

"The Company has good and marketable title to the real properties listed in Schedule [X], free from all mortgages, charges, liens, easements, rights of way, and other encumbrances except as disclosed. The Company has not received any notice of expropriation, planning restrictions, or building violations affecting the properties. All property registration fees and charges have been paid."

Dubai-specific issues: Verify ownership through Dubai Land Department, not merely through title deeds in the company's possession. Mortgages and other security interests should be disclosed with details of amounts secured and creditor consent requirements for share transfers.

Material Contracts and Change of Control

Change of control provisions in customer contracts, supplier agreements, and financing documents can destroy value immediately upon acquisition. These clauses may permit counterparties to terminate, renegotiate pricing, or demand additional security when share ownership changes.

Warranty drafting:

"Schedule [X] lists all Material Contracts. Except as disclosed in Schedule [X], none of the Material Contracts contains provisions that (i) require counterparty consent to the transactions contemplated by this Agreement, (ii) permit counterparty termination upon change of control, or (iii) allow material modification of terms upon change of ownership of the Company."

Define "Material Contract": Typically contracts with annual revenue/cost exceeding a threshold (e.g., AED 500,000), contracts with terms exceeding three years, exclusive arrangements, and contracts with related parties.

Disclosure expectations: Sellers must identify change of control provisions specifically. A general warranty that contracts are "in full force and effect" does not adequately allocate this risk. Buyers discovering undisclosed change of control provisions post-closing face uncertainty about whether warranty claims are available or whether the provisions were obvious upon contract review.

Tax Compliance in the Post-Corporate Tax Era

Since introduction of UAE Corporate Tax effective June 2023, tax warranties have become substantially more important in UAE M&A. Prior to corporate tax, UAE SPAs contained only VAT-related tax warranties. Now comprehensive corporate tax representations are standard.

Corporate tax warranty:

"The Company is registered for Corporate Tax with the Federal Tax Authority and holds Tax Registration Number [X]. The Company has timely filed all Corporate Tax returns required to be filed through [date] and has paid all Corporate Tax liabilities when due. The Company's Corporate Tax returns accurately reflect its taxable income calculated in accordance with Federal Decree-Law No. 47 of 2022. The Company has not received any tax assessments, notices of deficiency, or inquiries from the FTA regarding its Corporate Tax filings. The Company is [is not] a Qualifying Free Zone Person and [has/has not] derived Qualifying Income exceeding the de minimis threshold permitted under the Corporate Tax Law."

QFZP status risk: If the target claims Qualifying Free Zone Person status for 0% tax rate, this requires careful verification. As noted in our due diligence guide, companies often claim QFZP status without meeting all conditions. If status fails upon FTA audit, the company faces 9% tax on all taxable income, not just non-qualifying income. This exposure should be specifically indemnified.

Knowledge qualifications: Sellers resist absolute tax warranties, particularly regarding interpretation of recent legislation. Buyers should accept "to the Company's knowledge" qualifications for complex tax positions but define "knowledge" narrowly—typically limited to CFO, CEO, and finance director actual knowledge.

Purchase Price Mechanisms: Locked Box vs Completion Accounts

The purchase price mechanism determines how much the buyer ultimately pays and when that amount becomes fixed. Two methodologies dominate UAE private equity transactions, each allocating risk differently.

Locked Box Mechanism

Under a locked box structure, the purchase price is fixed at signing based on target company accounts as of a locked box date (typically the most recent month-end before signing). The economic benefit and risk of the business from the locked box date onward passes to the buyer, even though legal completion occurs later.

The SPA prohibits "leakage"—any value extraction by the seller or its affiliates between locked box date and completion. Permitted leakage (ordinary course dividends, salary, etc.) is specifically defined. Any unauthorized leakage reduces the purchase price on a dollar-for-dollar basis.

Advantages for buyers:

- Price certainty at signing

- No post-completion price adjustment disputes

- Seller cannot extract value between signing and closing

Advantages for sellers:

- No completion accounts negotiation

- No escrow retention for working capital disputes

- Faster completion with immediate payment

UAE market practice: Locked box has become increasingly common in UAE institutional M&A over the past five years, particularly in competitive auction processes where sellers want price certainty and buyers accept trading off completion accounts flexibility for deal certainty.

Key drafting points:

Locked box date definition: Must be clearly specified. "The unaudited management accounts of the Company as of 31 October 2025" is sufficient if those accounts exist and have been delivered to the buyer.

Permitted leakage list: Must be exhaustive. Typical permitted leakage includes:

- Salaries and bonuses to employees (excluding seller affiliates) in the ordinary course

- Routine operating expenses in the ordinary course

- Tax payments

- Specifically identified capital expenditure

- Disclosed dividends up to AED [X]

Leakage indemnity: The seller indemnifies the buyer for any leakage not permitted. This indemnity typically sits outside the general limitation on claims—no cap, no basket, no de minimis.

Example leakage clause:

"Seller shall procure that between the Locked Box Date and Completion, there shall be no Leakage from the Company. For purposes of this Agreement, 'Leakage' means any reduction in the consolidated net assets of the Company resulting from (i) declaration or payment of dividends or other distributions to shareholders, (ii) repayment of shareholder loans, (iii) management fees or other payments to shareholders or their affiliates, (iv) transfer of assets below fair market value, or (v) incurrence of liabilities for the benefit of shareholders or their affiliates, in each case other than Permitted Leakage specifically identified in Schedule [X]."

Completion Accounts Mechanism

Under completion accounts, the purchase price at signing is provisional (often based on a normalized or target level of working capital and net debt). After completion, the buyer prepares completion accounts determining actual working capital and net debt as of the completion date. The purchase price adjusts upward if working capital exceeds the target and downward if it falls short.

Advantages for buyers:

- Pay only for actual net assets delivered

- Protection against working capital deterioration between signing and completion

- Can reflect seasonal variations in working capital

Disadvantages for buyers:

- Post-completion price disputes are common

- Requires escrow retention pending finalization

- Seller may manipulate working capital before completion

Drafting considerations:

Working capital definition: Must be precise. Typically defined as consolidated current assets minus consolidated current liabilities, excluding specifically identified items (cash, debt, seller-related receivables/payables).

Accounting policies: Completion accounts must be prepared "in accordance with the Accounting Policies set out in Schedule [X], consistently applied." The schedule should specify the accounting basis (UAE GAAP, IFRS), treatment of specific items, and dispute resolution if policies are ambiguous.

Preparation and review timeline:

- Buyer prepares draft completion accounts within [30/45/60] days after completion

- Seller reviews and provides comments within [15/20] days

- Parties negotiate in good faith for [15/20] days

- If disagreement remains, refer to independent accountant for determination

Independent accountant determination: Should be binding and final, not subject to appeal except for manifest error. Specify that the accountant acts as expert, not arbitrator (this affects procedural rules and costs allocation). Identify potential accounting firms in advance.

Example adjustment mechanism:

"If Completion Working Capital exceeds Target Working Capital, the Purchase Price shall be increased by an amount equal to such excess. If Completion Working Capital is less than Target Working Capital, the Purchase Price shall be decreased by an amount equal to such shortfall. Any adjustment shall be paid [by Buyer to Seller] or [by Seller to Buyer (from Escrow)] within [5/10] Business Days of agreement on or determination of the Completion Accounts."

Conditions Precedent: Competition Clearance and Regulatory Approvals

Conditions precedent are events that must occur before the buyer is obligated to complete the purchase. They protect buyers from being forced to complete acquisitions where critical assumptions have not materialized.

UAE Competition Law Mandatory Filing

The most significant recent development in UAE M&A is the mandatory merger control regime under Federal Decree-Law No. 36 of 2023, effective March 31, 2025. Cabinet Decision No. 3 of 2025 sets the notification thresholds.

Filing requirement: Transactions where:

- Combined annual turnover in the UAE exceeds AED 300 million, OR

- Combined market share exceeds 40%

must be notified to the Ministry of Economy at least 90 days before completion.

Suspensory effect: The transaction cannot complete until approval is granted or the review period expires. Jumping the gun—completing before clearance—can result in fines of 2% to 10% of the acquirer's UAE revenues.

Timeline: The Ministry has 90 days to review (extendable by 45 days). If no decision is issued within the review period, the application is deemed rejected.

SPA drafting implications:

Competition clearance as condition precedent:

"Completion is conditional upon receipt of all necessary approvals, clearances, and consents from the Ministry of Economy under the Competition Law, or expiry of all applicable waiting periods, without any objections or conditions having been raised."

Timing coordination: If competition clearance is required, the signing-to-completion timeline extends by at least 90 days. Structure the transaction with signing subject to competition clearance, not closing subject to clearance (otherwise pre-emption procedures must be followed before filing can occur).

Failure to obtain clearance: Specify what happens if clearance is denied. Typically the buyer can walk away with no liability, but consider whether the seller should bear costs (due diligence expenses, financing commitment fees) if denial resulted from seller misrepresentation about market share.

Reverse break fee: In larger transactions, sellers may demand reverse break fees—amounts the buyer must pay if clearance is not obtained despite good faith efforts. These are rare in UAE M&A but are emerging in transactions exceeding AED 500 million where seller opportunity cost is substantial.

Sector-Specific Regulatory Approvals

Certain regulated sectors require pre-approval of ownership changes beyond standard DED registration.

Financial services: Share transfers in UAE banks, insurance companies, and other financial institutions regulated by the Central Bank or Securities and Commodities Authority require regulatory consent. Approval timelines can extend three to six months.

Healthcare: Private hospitals and clinics regulated by the Department of Health (Abu Dhabi) or Dubai Health Authority require approval of ownership changes. Medical professional licensing may be tied to ownership structure.

Education: Schools and universities require consent from the Knowledge and Human Development Authority (Dubai) or Department of Education and Knowledge (Abu Dhabi) for share transfers.

Media and telecom: These heavily regulated sectors have foreign ownership restrictions and require regulator approval.

Drafting approach: Make sector regulator approval an explicit condition precedent with specified timeline. Require the seller to use best efforts to obtain approval, including providing information and responding to regulator inquiries. Consider whether buyer needs ability to withdraw if approval is granted subject to unacceptable conditions.

Third-Party Consents

Beyond regulatory approvals, commercial contracts may require third-party consent for share transfers.

Key contracts requiring consent: Bank facilities (almost always require lender consent to change of control), major customer contracts, exclusive supplier arrangements, franchise and license agreements, leases for key premises.

Condition precedent vs covenant: Buyers must decide whether to make third-party consents conditions precedent (buyer can walk away if not obtained) or seller covenants (seller must use best efforts to obtain, but buyer must still complete if not obtained).

Market practice: For truly critical consents (e.g., bank facility providing working capital, lease for headquarters), make these conditions precedent. For less critical consents, treat as seller covenant with specific indemnity if loss results from failure to obtain consent.

Indemnities and Limitations on Liability

Warranty claims compensate buyers for breaches of seller representations. Indemnities go further—they provide specific protection for identified risks regardless of warranty breach, often with different limitation structures.

Structure of Limitations on Warranty Claims

Standard limitation structures in UAE private equity transactions follow international practice with some local adaptations.

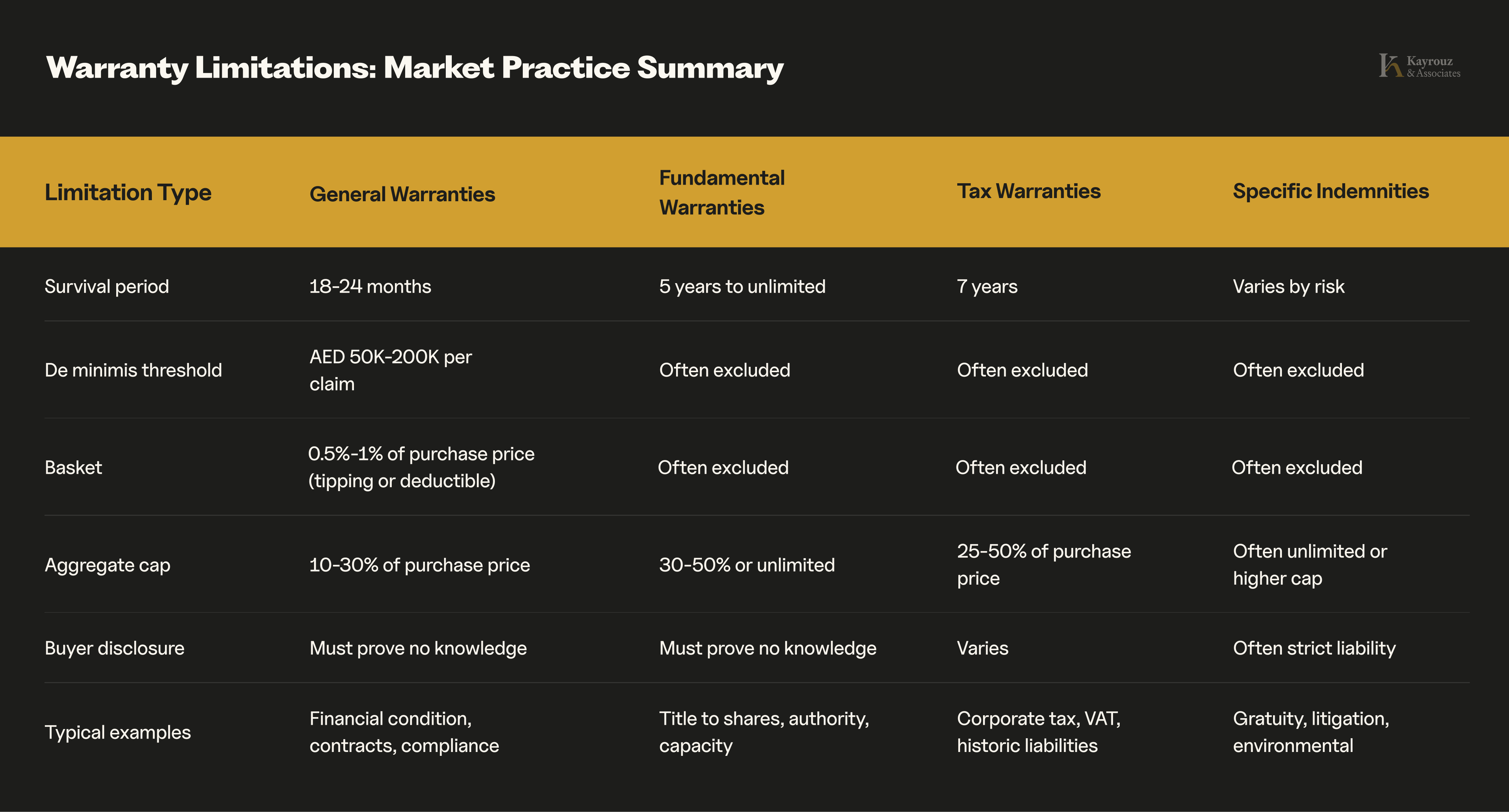

Time limits:

- General warranties: 18-24 months from completion (occasionally as short as 12 months in founder-led sales)

- Fundamental warranties: Longer survival, often the full statute of limitations period (currently 15 years for contractual claims under UAE Civil Code, though this seems likely to reduce)

- Tax warranties: Extended survival to cover FTA audit periods (typically seven years)

- Title warranties: Unlimited survival (seller always warrants it actually owns the shares sold)

Financial thresholds:

De minimis: Individual claims below a threshold amount (commonly AED 50,000-200,000) are disregarded entirely. This eliminates nuisance claims.

Basket: Claims only become payable once aggregate claims exceed a threshold amount (typically 0.5%-1% of purchase price). Two variants:

- Tipping basket: Once threshold is crossed, buyer recovers all losses from the first dollar

- Deductible basket: Buyer only recovers losses exceeding the threshold

Cap: Maximum aggregate liability is capped, typically at 10-30% of purchase price for general warranties. Fundamental warranties may have higher caps (30-50%) or no cap.

Warranty Limitations: Market Practice Summary

Note: "Excluded" means the threshold does not apply - claims can be made without meeting de minimis or basket requirements, and may not count toward the cap.

Example limitation structure:

"Seller shall have no liability for Warranty Claims unless:(a) the Claim Amount of an individual Warranty Claim exceeds the De Minimis Amount specified in Schedule A; and(b) the aggregate Claim Amounts of all Warranty Claims exceed the Basket Amount specified in Schedule A, in which case Buyer may recover all Warranty Claims from the first dollar;provided that:(i) the aggregate liability of Seller for all Warranty Claims shall not exceed the Cap Amount specified in Schedule A;(ii) the De Minimis Amount, Basket, and Cap do not apply to Fundamental Warranties, Tax Warranties, or Specific Indemnities as defined in this Agreement;(iii) Warranty Claims must be notified within 18 months of Completion, except Fundamental Warranties (no time limit) and Tax Warranties (7 years)."

Tax Indemnities

Tax indemnities warrant specific attention in UAE M&A following introduction of corporate tax. These indemnities provide absolute protection for pre-completion tax liabilities and are typically structured outside the general warranty limitation framework.

Comprehensive tax indemnity:

"Seller shall indemnify and hold harmless Buyer and the Company from and against any Tax Liability (as defined below) arising from or in connection with:(a) any taxable period or portion thereof ending on or before Completion;(b) any transaction, event, or omission occurring on or before Completion;(c) any breach of Tax Warranties contained in this Agreement;(d) failure to comply with Tax obligations on or before Completion;(e) any assessment, adjustment, or challenge by the Federal Tax Authority relating to any pre-Completion period.

For this purpose, 'Tax Liability' includes the Tax itself, penalties, interest, professional fees incurred in responding to Tax Authority inquiries or disputes, and court or arbitration costs."

Allocation of Tax liabilities: Specify how to allocate Tax for "straddle periods" (periods beginning before and ending after Completion). UAE corporate tax is annual, so this is less complex than in jurisdictions with interim filing requirements, but FTA audits can span multiple years.

Buyer covenant: Buyers typically covenant not to take any action post-Completion that would increase pre-Completion Tax liabilities without seller consent. This includes limitations on amending historical Tax returns, changing accounting methods retrospectively, or taking positions in current periods that affect prior periods.

Specific Indemnities

Beyond warranty claims and tax, SPAs typically include specific indemnities for identified risks that due diligence revealed but could not be quantified or eliminated.

Common specific indemnities:

Litigation: Known disputes or regulatory proceedings identified during due diligence are specifically indemnified, often with the full exposure amount rather than just the cap amount.

Environmental liabilities: If contamination or environmental non-compliance is discovered, seller indemnifies for remediation costs.

Intellectual property claims: If due diligence identified potential IP infringement, seller provides specific protection.

Undisclosed related party transactions: Protection against historical related party arrangements that surface post-completion.

Gratuity underprovisioning: As discussed, many buyers require specific indemnity for gratuity shortfalls with higher or unlimited caps.

W&I Insurance Availability

Warranty and indemnity insurance—where an insurer assumes seller warranty liability—has been available in UAE M&A for approximately five years. International insurers including AIG, Liberty, and AXA XL provide coverage.

When W&I insurance makes sense:

- Founder-led sales where founders have limited ability to provide escrows

- Competitive auctions where clean exit is attractive to sellers

- Management buyouts where management has limited capital

Practical considerations: W&I insurance requires robust due diligence, as insurers exclude known issues. The buyer typically pays the premium (1-2% of cover amount). Coverage commonly provides 10-30% of purchase price for 3-7 years.

UAE-specific issues: Insurers are still developing comfort with UAE legal risk, and certain exposures may be excluded or subject to significant retentions. Obtain insurer engagement early to understand coverage scope and inform SPA negotiation.

Material Adverse Change Clauses

MAC (or material adverse effect—MAE) clauses allow buyers to walk away from signed transactions if specified adverse events occur before completion. They are rare in UAE M&A outside of transactions with extended signing-to-closing periods or cross-border deals with substantial regulatory approval timelines.

What Constitutes MAC Under UAE Law

UAE commercial law does not define material adverse change. The DIFC Courts have addressed MAC clauses in several disputes, drawing on English common law precedent.

The key principle: MAC clauses are construed narrowly. They protect buyers only against truly fundamental changes affecting the business as a whole, not ordinary commercial volatility or events the buyer could have anticipated.

DIFC Courts approach: In determining whether an MAC has occurred, courts examine:

- Whether the adverse effect is material (measured both quantitatively and qualitatively)

- Whether the effect is on the company as a whole or merely one division/product

- Whether the effect is likely to be long-term rather than temporary

- Whether the event was foreseeable at signing

COVID-Era Developments in MAC Interpretation

The pandemic generated significant MAC litigation globally, including disputes in the DIFC Courts. Based on published decisions and market practice, several principles have emerged in how courts and arbitrators assess MAC claims:

- General economic deterioration affecting entire sectors does not necessarily constitute MAC if specifically excluded in the MAC definition, even where impacts are severe

- MAC must affect the target specifically, not merely reflect general market conditions that impact all industry participants similarly

- Financial performance declines must be measured against reasonable expectations and comparable company performance

- Short-term disruptions, even if substantial, may not qualify as MAC if recovery is reasonably expected within the contract's contemplated timeframe

Drafting MAC Clauses

MAC clauses in UAE SPAs typically follow this structure:

Positive definition:

"Completion is conditional upon no Material Adverse Change having occurred between signing and Completion. For purposes of this Agreement, 'Material Adverse Change' means any change, event, occurrence, or development that has had or would reasonably be expected to have a material adverse effect on the business, operations, financial condition, prospects, or assets of the Company, taken as a whole."

Materiality threshold: Consider specifying a quantitative threshold (e.g., "reduction in EBITDA by more than [20]% compared to prior year") combined with qualitative assessment.

Excluded events: Comprehensive MAC definitions exclude events that buyers should bear risk for:

"Notwithstanding the foregoing, none of the following shall constitute or be considered in determining whether a Material Adverse Change has occurred:(a) changes in general economic, financial, or capital market conditions;(b) changes affecting the industry in which the Company operates generally;(c) changes in laws or regulations of general applicability;(d) acts of war, terrorism, natural disasters, or pandemics;(e) changes resulting from announcement of the Transaction;(f) failure to meet financial projections (though underlying causes may constitute MAC);(g) changes resulting from actions taken at Buyer's request or with Buyer's consent;

provided that the events described in clauses (a) through (d) may constitute a MAC to the extent they disproportionately affect the Company relative to other participants in the industry."

Seller knowledge: Some sellers argue MAC should be limited to matters within seller's knowledge. Buyers resist this—the point of MAC is to protect against unknown adverse developments. Knowledge qualifications substantially undermine MAC protection.

Burden of proof: Specify who bears burden of establishing whether MAC occurred. Market practice places this burden on the party asserting MAC (typically the buyer seeking to avoid completion).

Restrictive Covenants: Non-Compete and Non-Solicit

Restrictive covenants prevent sellers from competing with the business sold or soliciting customers, employees, and suppliers. These provisions protect the buyer's investment by ensuring the seller cannot immediately undermine the goodwill and relationships purchased.

UAE Law Constraints on Non-Compete

UAE courts apply a reasonableness and public policy test when assessing non-compete provisions. The enforceability analysis differs depending on whether the restriction applies to employees or to seller-shareholders in M&A transactions.

For employee non-competes, Federal Decree-Law No. 33 of 2021 (UAE Labour Law), Article 10, caps the maximum duration at two years and requires the restriction to be necessary to protect the employer's legitimate interests.

For seller non-competes in M&A, courts assess reasonableness based on:

Duration: Courts typically accept 12-24 months as reasonable for seller-shareholders exiting the business entirely. Longer periods face enforceability challenges unless substantial consideration is provided.

Geographic scope: Must be limited to areas where the company actually operates. "The United Arab Emirates" is generally acceptable for companies operating across the UAE. "Middle East" or "GCC" may be enforceable if the target conducts substantial business in those markets.

Activity scope: Must be limited to businesses that directly compete with the target's business. Broadly worded prohibitions on "any business activity" are unenforceable.

Reasonableness standard: UAE courts assess whether the restriction is necessary to protect the buyer's legitimate business interests versus whether it imposes unreasonable hardship on the seller. Blanket prohibitions that would prevent the seller from earning a livelihood are struck down.

Practical Enforceability Issues

Even well-drafted non-compete provisions face enforcement challenges in the UAE.

Injunctions are difficult to obtain. UAE courts are generally reluctant to grant interim injunctions restraining breaches of non-compete provisions. The court typically requires the applicant to demonstrate immediate and irreparable harm that cannot be adequately compensated by damages. Sellers who breach non-compete provisions can often continue competing for extended periods while cases progress through courts.

Damages require proving loss. To recover damages for non-compete breach, the buyer must prove actual financial loss resulting from the breach. "But for" causation must be established. If the buyer's business declines after the seller establishes a competing business, the buyer must prove the decline resulted from seller competition rather than market conditions, buyer mismanagement, or other factors.

Blue pencil doctrine application is uncertain. In some jurisdictions, if a non-compete provision is overbroad, courts will "blue pencil" it—striking excessive portions while enforcing reasonable elements. UAE courts' willingness to do this varies. Some judges will refuse to enforce any provision they consider unreasonable rather than modifying it to make it reasonable.

Liquidated Damages Provisions

Given enforcement difficulties, many UAE SPAs include liquidated damages provisions specifying predetermined compensation for non-compete breaches.

Example:

"If Seller breaches the non-compete covenant in Clause [X], Seller shall pay to Buyer liquidated damages in the amount of AED [Y] for each month or part thereof during which the breach continues, such amount being the parties' genuine pre-estimate of Buyer's loss resulting from such breach and not a penalty."

Enforceability considerations: UAE courts will enforce liquidated damages if the amount is a reasonable pre-estimate of loss. Amounts that are clearly punitive (substantially exceeding plausible actual loss) may be reduced by courts exercising equitable powers.

Practical impact: Liquidated damages provisions do not prevent breach, but they create financial consequences that may deter breach or at least provide compensation without needing to prove actual loss.

Non-Solicit Provisions

Non-solicit provisions—prohibiting solicitation of customers, employees, and suppliers—face fewer enforcement challenges than non-compete obligations because they do not prevent sellers from working, merely from targeting specific relationships.

Customer non-solicit:

"For [18/24] months from Completion, Seller shall not, directly or indirectly:(a) solicit or accept business from any person who was a customer of the Company during the 12 months preceding Completion;(b) induce or attempt to induce any such customer to reduce, terminate, or not renew business with the Company;(c) interfere with the Company's relationships with its customers."

Employee non-solicit:

"For [12/18/24] months from Completion, Seller shall not, directly or indirectly:(a) solicit, recruit, or hire any employee of the Company;(b) induce or encourage any employee to leave employment with the Company;(c) assist any third party in recruiting Company employees."

Practical tip: Define "employee" to include individuals employed during [12] months before Completion, not just those employed at Completion. This prevents sellers from recruiting employees who resign immediately after Completion.

Different Treatment for Sellers vs Management

SPAs should differentiate between restrictions on selling shareholders versus management team members who roll equity forward.

Selling shareholders exiting entirely: Apply standard non-compete (1-2 years) and non-solicit (18-24 months) provisions.

Founders or management continuing in employment: More nuanced restrictions are necessary. These individuals need to continue working for the business, so blanket non-competes are inappropriate. Instead, include:

- Non-compete applies only if they resign or are terminated for cause

- Non-compete duration tied to employment continuation (no restriction while employed; 12 months after departure)

- Exceptions for certain permitted activities

- Consideration for restrictions (salary continuation, restricted stock vesting)

Signing vs Completion: Managing the Interim Period

In transactions with conditions precedent—competition clearance, regulatory approvals, third-party consents—a gap exists between signing the SPA and completing the transaction. This interim period creates risk that the business deteriorates or the seller extracts value before the buyer takes control.

Conduct of Business Covenants

Conduct of business covenants require the seller to procure that the target operates in the "ordinary course of business consistent with past practice" between signing and completion. These provisions preserve the business the buyer agreed to purchase.

Standard conduct of business covenant:

"Between signing and Completion, Seller shall procure that the Company:(a) conducts its business in the ordinary course consistent with past practice;(b) uses commercially reasonable efforts to preserve its business organization, retain key employees and customers, and maintain supplier and other business relationships;(c) maintains insurance coverage at current levels;(d) complies with all applicable laws and regulations;(e) maintains books and records in accordance with past practice."

Prohibited Actions

Beyond the general ordinary course obligation, SPAs specifically prohibit certain actions without buyer consent:

Capital structure changes:

- No amendments to constitutional documents

- No issuance of new shares or securities

- No share repurchases or redemptions

- No dividends or distributions (except as specifically permitted)

Financial commitments:

- No incurrence of debt exceeding AED [X]

- No capital expenditure exceeding AED [Y]

- No acquisitions or disposals of assets outside ordinary course

- No entry into material contracts

Employee matters:

- No salary increases exceeding [%]

- No new employee hires in management positions without consultation

- No terminations of key employees

- No changes to employee benefit plans

Related party transactions:

- No new transactions with seller or its affiliates

- No amendments to existing related party arrangements

Tax matters:

- No tax elections or changes in tax accounting methods

- No settlement of tax disputes without buyer consultation

Seller Access and Information Rights

During the interim period, buyers need visibility into business performance and developments to assess whether MAC has occurred and whether conditions will be satisfied.

Standard access provision:

"Between signing and Completion, Seller shall:(a) provide Buyer and its representatives reasonable access during business hours to the Company's premises, books, records, and senior management;(b) deliver monthly management accounts within [10] Business Days of month-end;(c) promptly notify Buyer of any material adverse change, litigation, or regulatory inquiry;(d) provide any additional information reasonably requested by Buyer in connection with finalizing financing arrangements or regulatory filings;(e) cooperate in Buyer's preparation for transition and integration."

Confidentiality reminder: Access provisions typically remind parties that confidentiality obligations in the NDA or SPA continue to apply.

Buyer Obligations During Interim Period

Buyers are not passive during the interim period. They have obligations to pursue satisfaction of conditions.

Efforts standard: SPAs typically require buyer to use "best efforts" or "commercially reasonable efforts" to obtain regulatory approvals and satisfy financing conditions. The distinction matters:

- Best efforts: Buyer must take all reasonable steps to achieve the objective, potentially including significant cost or operational impact

- Commercially reasonable efforts: Buyer must take reasonable steps but is not required to incur disproportionate expense or make business concessions

Specific buyer obligations commonly include:

- Timely filing of competition notifications

- Responding to regulator requests for information

- Finalizing financing arrangements (if completion is conditional on financing)

- Obtaining internal approvals (board, investment committee)

- Cooperating in obtaining third-party consents

Execution Mechanics: Notarization and Registration

The execution phase—moving from signed SPA to registered share transfer—involves procedural steps that frequently surprise international acquirers unfamiliar with UAE requirements.

Signing the English SPA

The long-form English SPA typically signs first. Parties can sign in counterpart (separate copies of the signature page), electronically, and remotely. Under UAE law, electronic signatures are valid if they meet requirements for authenticating the signatory.

Signing the English SPA creates contractual obligations between the parties but does not transfer shares under UAE law.

Preparing for Notarization

Before attending the notary, several preparatory steps must be completed:

Arabic transfer agreement preparation: Engage a licensed translator to prepare the short-form Arabic transfer agreement accurately reflecting SPA commercial terms. The Arabic document should be reviewed by Arabic-speaking legal counsel to ensure consistency with the English SPA.

Power of attorney execution: If parties will not personally attend notarization, powers of attorney must be prepared. For foreign corporate buyers, this requires:

- Board resolution authorizing execution of the power of attorney

- Execution of the power of attorney

- Notarization in the home jurisdiction

- Legalization through the UAE embassy in the home jurisdiction

- Attestation by UAE Ministry of Foreign Affairs

- Certified Arabic translation

This process can take 2-4 weeks and causes many transaction delays.

DED pre-clearance: Some buyers obtain initial DED clearance before attending notarization. The DED can confirm whether the proposed transaction is permissible and identify missing documentation before the notary appointment is scheduled.

The Notarization Process

Notarization occurs at designated notary offices in Dubai (typically at the Notary Public Office in the Courts complex) or through private notaries for certain transaction types.

What happens at notarization:

- All parties or their authorized representatives appear with original identification

- The notary verifies identity and authority

- The Arabic transfer agreement is read (in Arabic)

- Parties confirm their consent to the terms

- Parties sign the Arabic agreement in the notary's presence

- The notary authenticates the signatures and notarizes the document

- The notarized document is issued with an official stamp and reference number

Duration: The appointment typically takes 30-60 minutes for straightforward share transfers.

Critical understanding: As discussed earlier, notarization creates binding legal effect under UAE law. The shares transfer at notarization, not at a separate "closing." This timing is crucial for managing conditions precedent and payment mechanics.

Post-Notarization Registration

After notarization, the transaction must be registered with the DED to update the commercial register and trade license. In Dubai mainland LLC closings, the Arabic deed and DED registration steps are where delays most commonly occur despite parties believing execution would be straightforward.

Registration process:

- Submit notarized Arabic transfer agreement

- Submit updated constitutional documents reflecting new ownership

- Pay registration fees (typically ranging from AED 1,000 to AED 5,000 depending on company size and amendments required)

- Obtain updated trade license

Timeline: DED registration often completes within 3-10 business days after submission of complete documentation, though processing times can extend during peak periods or if additional documentation is requested.

Practical consideration: The updated trade license is required for the buyer to exercise control over bank accounts, change authorized signatories, and update regulatory registrations. Plan for this administrative period when scheduling transition activities.

Common Execution Failures

Several issues frequently cause problems at the execution stage:

Incomplete document legalization: Foreign corporate buyers often underestimate the time required to legalize powers of attorney and corporate documents. Transactions scheduled to close on specific dates miss deadlines because legalization is not complete.

Discrepancies between English SPA and Arabic transfer: If material terms differ between documents, the notary may refuse to proceed. More problematically, if differences exist but notarization proceeds, disputes can arise later about which document governs.

Pre-emption procedures not completed: If statutory pre-emption rights were not properly addressed (notification to other shareholders, waiting period expiration, waivers obtained), the transfer may be challenged post-completion.

Seller fails to attend: If the seller or authorized representative does not appear at notarization, the transaction cannot complete on the scheduled date. SPAs should address consequences of seller non-appearance.

Payment timing issues: Confusion about when payment is due relative to notarization can cause disputes. Clarify in the SPA whether payment occurs (a) before notarization, (b) immediately after notarization, or (c) after DED registration and trade license issuance. Payment methods (wire transfer, bank draft, escrow release) should be specifically addressed.

Dispute Resolution: Arbitration vs Litigation for SPA Disputes

Disputes arising from share purchase agreements involve substantial amounts (often 10-30% of purchase price for warranty claims), require expertise in commercial and M&A law, and benefit from confidentiality. The choice of dispute resolution mechanism significantly affects outcomes.

Why Arbitration Dominates UAE M&A

Arbitration has become the standard dispute resolution choice for institutional M&A in the UAE for several reasons:

Confidentiality: Arbitration proceedings and awards are confidential. For private companies and private equity funds, this avoids public disclosure of valuations, financial performance, and dispute details.

Expertise: Parties can select arbitrators with specific M&A experience. UAE courts assign cases to judges without regard to specialization, and commercial disputes may be heard by judges with limited M&A background.

International enforceability: Arbitral awards are enforceable in over 160 countries under the New York Convention. Court judgments face more complex enforcement procedures.

Flexibility: Arbitration allows parties to tailor procedures—language, document production, hearing schedules, representation rules—to suit commercial needs.

Finality: Arbitral awards are generally not appealable (absent very limited grounds). Court decisions go through multiple appeal levels, extending disputes for years.

DIAC Arbitration with DIFC Seat

The combination that has emerged as market standard for UAE M&A disputes is arbitration under Dubai International Arbitration Centre (DIAC) rules with the seat of arbitration in the Dubai International Financial Centre (DIFC).

Why this combination works:

DIAC rules: Familiar to regional practitioners, efficient timelines (often 6-15 months from constitution of tribunal to award depending on case complexity), reasonable costs compared to international institutions, emergency arbitrator provisions for urgent interim relief.

DIFC seat: Provides the DIFC Courts as supervisory authority with power to grant interim measures, address challenges to awards, and enforce awards. DIFC Courts apply common law principles, conduct proceedings in English, and have established arbitration-friendly jurisprudence.

Example clause:

"Any dispute arising out of or in connection with this Agreement, including any question regarding its existence, validity, or termination, shall be referred to and finally resolved by arbitration under the DIAC Arbitration Rules. The seat of arbitration shall be the Dubai International Financial Centre. The tribunal shall consist of [one/three] arbitrator(s). The language of the arbitration shall be English."

Three-arbitrator vs single arbitrator: For disputes with potential value exceeding AED 10 million, three arbitrators provide greater confidence in outcome quality and reduce concerns about individual arbitrator bias. For smaller disputes, single arbitrators reduce costs and expedite proceedings.

Emergency Arbitrator Provisions

SPA disputes sometimes require urgent relief before the tribunal is constituted—preventing seller from disposing of assets, enforcing confidentiality obligations, or preserving evidence.

DIAC rules include emergency arbitrator procedures allowing a party to seek interim measures within 15 days of filing the request for arbitration, well before the main tribunal is appointed.

Emergency arbitrator relief is available for:

- Preserving status quo

- Taking action to prevent current or imminent harm

- Preserving assets that may be needed to satisfy award

- Preventing destruction or deterioration of evidence

Example provision incorporating emergency arbitrator:

"The parties agree that the emergency arbitrator provisions in Article 21 of the DIAC Arbitration Rules apply to this Agreement. Pending constitution of the arbitral tribunal, either party may apply to the emergency arbitrator for interim or conservatory measures."

Governing Law vs Seat of Arbitration

A common misunderstanding: governing law and seat of arbitration serve different functions and need not match.

Governing law determines the substantive legal rules applied to interpret the contract and determine parties' rights and obligations. For UAE M&A involving international buyers, common choices are English law, DIFC law, or UAE law.

Seat of arbitration determines the procedural law governing the arbitration (how hearings are conducted, what procedural rules apply, what court has supervisory jurisdiction). The seat is DIFC in the standard clause above.

Can you have English law as governing law with DIFC as seat? Yes. The tribunal applies English substantive law to the contract but follows DIFC procedural rules and benefits from DIFC Courts as supervisory authority.

Common Negotiation Points in UAE Private Equity Deals

Negotiation dynamics in UAE private equity transactions follow patterns that have emerged as market practice over the past decade. Understanding these patterns helps identify which issues merit expenditure of negotiation capital and which reflect market consensus.

Seller-Favorable vs Buyer-Favorable Positions

Understanding market practice on key negotiation points helps parties identify which terms merit expenditure of negotiating capital and which reflect consensus positions that rarely move.

SPA Negotiation: Seller vs Buyer Positions

Key insight: Market practice has shifted toward seller-favorable terms in competitive auctions where multiple bidders compete. Negotiated transactions between single buyer and willing seller typically achieve more balanced outcomes.

Points Worth Fighting For (Buyer Perspective)

Gratuity indemnity: Under-provisioned gratuity is near-universal in UAE targets. Insist on independent calculation, full disclosure, and specific indemnity with extended survival and higher cap.

Tax indemnity scope: Post-corporate tax introduction, tax indemnities have become critical. Ensure comprehensive coverage of pre-completion periods with appropriate time limits (aligned with FTA audit period).

Key contract change of control: Identify top 5-10 customers by revenue and ensure change of control provisions are disclosed. Consider making consent from these key customers a condition precedent if they represent >30% of revenue.

Emiratisation compliance: Penalties accumulate quickly. Obtain specific warranties on current compliance status and consider specific indemnity for historical non-compliance.

QFZP status if applicable: If target claims Qualifying Free Zone Person status, verify rigorously and obtain specific indemnity with unlimited cap if status fails.

Points Worth Conceding (Buyer Perspective)

Fundamental warranty survival: Sellers often resist unlimited survival for fundamental warranties. Accepting 5-year survival rather than unlimited for title and capacity warranties is reasonable—these matters will be discovered quickly if problems exist.

Knowledge qualifications on forward-looking matters: Warranties about future regulatory compliance or absence of future adverse events can reasonably be qualified with seller knowledge. Resist knowledge qualifications on current factual matters.

Certain disclosure basket items: If the disclosed matter is immaterial and properly quantified, accepting that it falls outside warranty protection is reasonable rather than fighting to include it under the basket.

Seller continuing involvement post-completion: If the seller or founder is essential for business continuity and will remain as employee, accommodating reasonable requests around their employment terms and equity participation can preserve deal dynamics.

Management Equity Rollovers

In management buyouts or transactions where management rolls equity forward, additional negotiation points arise:

Vesting schedules: PE funds typically require management equity to vest over 3-4 years, incentivizing continued employment. Management prefers shorter vesting or immediate vesting.

Good leaver/bad leaver definitions: Carefully negotiate what constitutes "good leaver" (death, disability, retirement, termination without cause) versus "bad leaver" (cause termination, voluntary resignation, competition). The valuation discount for bad leavers can be substantial (often 50-75% of fair value).

Drag-along rights: Management equity is subject to drag-along—if PE fund sells, management must sell. Management should negotiate for minimum price thresholds or IRR hurdles before drag-along applies.

Board representation: Whether management receives board seats or merely observer rights affects influence over business decisions and exit timing.

Frequently Asked Questions

Is a share purchase agreement valid in English in the UAE?

Yes. The long-form share purchase agreement can be drafted in English, governed by English law, DIFC law, or UAE law, and does not require notarization. However, UAE law requires a separate Arabic transfer agreement to be executed before a notary to effect the actual share transfer in UAE mainland LLCs. Both documents are legally valid and serve different functions.

Do I need notarization to transfer shares in a Dubai mainland LLC?

Yes. Share transfers in Dubai mainland limited liability companies require execution of an Arabic transfer agreement before a UAE notary public, followed by registration with the Department of Economic Development. The notarization creates binding legal effect under UAE law. Free zone entities may have different requirements depending on the specific free zone.

When is UAE merger control filing required?

Under Federal Decree-Law No. 36 of 2023 and Cabinet Decision No. 3 of 2025, mandatory pre-closing notification to the Ministry of Economy is required when the transaction involves parties whose combined annual turnover in the UAE exceeds AED 300 million OR whose combined market share exceeds 40%. Filing must occur at least 90 days before completion, and the transaction cannot close until approval is granted or the review period expires.

What happens if conditions precedent are not satisfied?

If conditions precedent specified in the SPA (such as competition clearance or third-party consents) are not satisfied by the longstop date, either party can typically walk away without liability. However, if parties proceed to notarization before conditions are satisfied, the transfer may become binding under UAE law regardless of the English SPA conditions. This is why timing coordination is critical.

Can sellers limit their warranty liability to knowledge?

Knowledge qualifications on warranties are negotiable. Buyers typically resist knowledge qualifications for factual matters within seller control (such as whether contracts exist, assets are owned, or licenses are valid). Knowledge qualifications are more readily accepted for complex matters like tax positions or forward-looking regulatory compliance. The scope of "knowledge" should be clearly defined (typically limited to senior management actual awareness, not constructive knowledge).

How long do warranty claims survive after completion?

Market practice in UAE M&A typically provides 18-24 months survival for general warranties, though this is negotiable. Fundamental warranties (title to shares, authority to enter into transaction) often have longer survival or no time limit. Tax warranties commonly survive for seven years to cover Federal Tax Authority audit periods. Specific indemnities may have different survival periods depending on the risk addressed.

What is the difference between locked box and completion accounts?

Locked box fixes the purchase price at signing based on target accounts as of a specified date, with economic risk passing to buyer from that date. Any value extraction by seller between locked box date and completion (leakage) reduces the price. Completion accounts involve a provisional purchase price at signing with post-completion adjustment based on actual working capital and net debt delivered at closing. Locked box provides price certainty; completion accounts ensure buyer pays for what is actually delivered.

Can non-compete provisions be enforced in UAE courts?

Non-compete provisions are enforceable in the UAE if reasonable in duration, geographic scope, and activity scope. For employee non-competes, UAE Labour Law (Federal Decree-Law No. 33 of 2021, Article 10) caps duration at two years. For seller non-competes in M&A, courts assess reasonableness but enforcement through injunctions is difficult. Including liquidated damages provisions for breaches provides more practical protection than relying solely on injunctive relief.

Pre-Signing and Pre-Completion Checklist

Before Signing the SPA

Buyer actions:

- Due diligence substantially complete with all critical matters investigated

- Financing committed (equity commitment letters from fund LPs, debt commitment letters from lenders if applicable)

- Internal approvals obtained (investment committee, board as required)

- Competition analysis completed to determine if filing required

- Key third-party consents identified and strategy for obtaining developed

- Draft SPA and disclosure letter reviewed and negotiated

- Escrow arrangements agreed (escrow agent appointed, escrow terms documented)

Seller actions:

- Board and shareholder approvals for sale obtained

- Financial statements and disclosure materials prepared

- Disclosure letter finalized with legal counsel

- Other shareholders informed and pre-emption waivers obtained if required

- Notification to employees and key stakeholders planned (but not executed until signing announced)

Between Signing and Completion

Buyer actions:

- Competition filing submitted (if required) within required timeline

- Regulatory approval applications submitted

- Third-party consent requests delivered

- Financing documentation finalized

- Integration planning commenced

- Communication strategy for employees, customers, and suppliers developed

Seller actions:

- Operate business in ordinary course per conduct of business covenants

- Provide monthly management accounts and updates to buyer

- Cooperate in buyer's regulatory filings and integration planning

- Notify buyer immediately of any material adverse changes or covenant breaches

- Maintain insurance coverage and protect assets

Before Attending Notarization

Documentation readiness:

- All conditions precedent satisfied or waived in writing

- Arabic transfer agreement prepared and reviewed for consistency with English SPA

- Powers of attorney executed, legalized, attested, and translated (if parties not attending personally)

- Corporate documents (board resolutions, certificates of good standing, commercial register extracts) obtained

- Constitutional document amendments prepared for DED filing

- Payment arrangements confirmed and tested

DED preliminary review:

- Submit documents to DED for preliminary review

- Address any DED comments or requests for additional documentation

- Confirm no regulatory obstacles to registration

Confirmation calls:

- Buyer confirms financing is available and payment will be made on time

- Seller confirms no MAC has occurred and all representations remain accurate

- Legal counsel confirms all documentation is in order and all parties understand mechanics

How Kayrouz & Associates Structures UAE M&A Transactions

Share purchase agreements represent the single most important transaction document in any acquisition, and getting them right requires understanding both international M&A best practices and UAE legal and commercial realities.

Our corporate and commercial team has structured and executed complex UAE acquisitions across technology, healthcare, logistics, manufacturing, and financial services sectors. We represent institutional buyers (private equity funds, sovereign wealth funds, corporate acquirers) and sellers (founders, family businesses, portfolio companies) in negotiated transactions and competitive auctions.

Transaction Documentation and Execution

SPA Drafting and Negotiation: We prepare comprehensive share purchase agreements incorporating UAE-specific protections that international templates miss—Emiratisation warranties, WPS compliance representations, gratuity indemnification, QFZP status verification, and Arabic documentation coordination. For sellers, we negotiate limitations on liability, disclosure strategies, and warranty qualifications that appropriately allocate risk.

Bilingual Execution Support: We coordinate the relationship between English SPAs and Arabic transfer agreements, attend notarization proceedings, and manage DED registration through to updated trade license issuance. Our presence reduces execution risk and provides immediate problem-solving capacity.

Due Diligence Integration: Our due diligence services identify risks that must be addressed through SPA warranties, indemnities, and specific protections. We quantify exposures and recommend allocation approaches.

Competition and Regulatory Clearance: We prepare and file mandatory competition notifications, respond to Ministry of Economy information requests, and coordinate timing with transaction execution. For sector-specific approvals (financial services, healthcare, education), we manage the regulatory approval process.

Post-Completion Support

Warranty and Indemnity Claims: We advise buyers on breach quantification, notification requirements, and recovery strategy. We draft claims notices, evaluate seller defenses, and pursue resolution through negotiation or formal proceedings.

Dispute Resolution: We represent clients in DIAC arbitration and other proceedings involving SPA disputes, handling all aspects from statement of claim through final award and enforcement. Our team includes arbitrators and counsel experienced in complex commercial arbitrations.

Post-Acquisition Integration: We assist with shareholder agreement implementation for minority investments, board appointment coordination, and constitutional document alignment.

Download: UAE Share Transfer Closing Checklist

We have prepared a comprehensive checklist covering DED procedures, notarization requirements, MOA amendments, and common execution issues. Contact us to receive the checklist and discuss your transaction.

Related Capabilities

- Employment law advice on workforce matters, gratuity calculations, and MOHRE compliance

- Corporate tax structuring and controversy for post-2023 regime

- Intellectual property assessment and transfer for technology and brand-heavy businesses

- Real estate due diligence for property-intensive acquisitions

Contact our corporate and commercial team to discuss your UAE M&A transaction requirements.

Your success starts with the right guidance.

Whether it’s business or personal, our team provides the insight and guidance you need to succeed.