The UAE's tax system is getting stricter. Not in rates. In enforcement.

Federal Decree-Law No. 17 of 2025 rewrites the Tax Procedures Law. Federal Decree-Law No. 16 of 2025 amends the VAT Law. Both take effect January 1, 2026. The corporate tax rate stays at 9%. What changes is how the Federal Tax Authority operates: tighter deadlines, broader audit powers, and new rules that can wipe out VAT credits you assumed were safe.

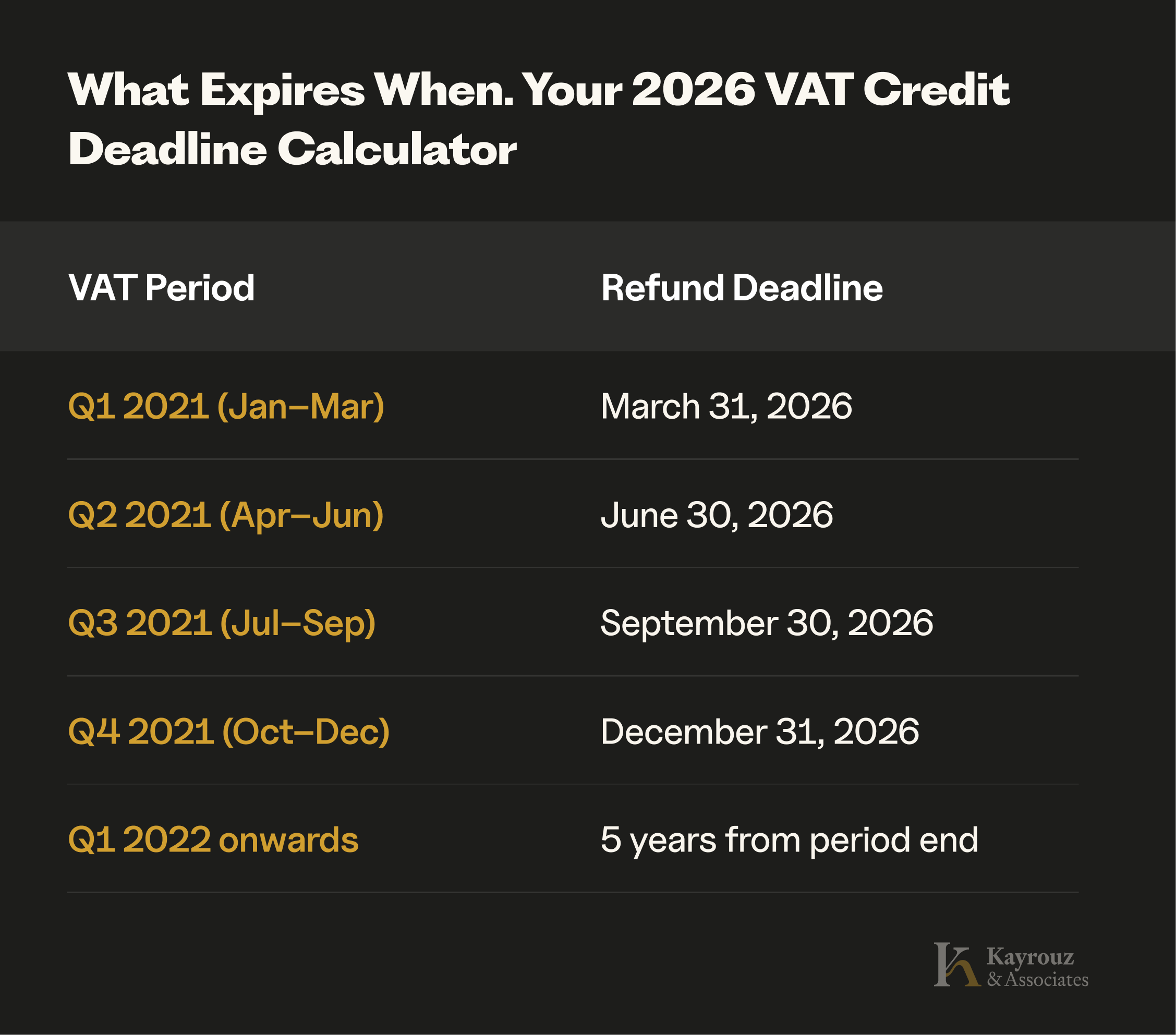

The most immediate problem is this: VAT credits from 2021 will start expiring in 2026. If you have been carrying forward excess input VAT without claiming refunds, some of that money may be gone by year-end.

If you manage multiple entities or have complex tax positions across free zones and mainland, we can review your filings, credit balances, and transfer pricing documentation on a monthly retainer. Contact our corporate team to discuss.

This article covers what is changing, what it means, and what to do about it.

The Five-Year Rule

The biggest procedural change is a hard deadline on refund claims.

Under the amended Tax Procedures Law, taxpayers have five years from the end of the relevant tax period to request a refund or use a credit balance to offset other liabilities. After that, the credit expires.

This applies to Corporate Tax, VAT, and Excise Tax. The clock starts at the end of the tax period when the credit arose.

For VAT, this creates an immediate problem. Many businesses have been carrying forward excess input VAT for years without claiming refunds. That was fine under the old rules. Under the new rules, credits more than five years old are gone.

A business that overpaid VAT in Q1 2021 has until Q1 2026 to claim it back. Miss that window and the money stays with the FTA.

The transitional provisions offer some relief. If the five-year period for a credit balance already expired before January 1, 2026, or will expire within one year after that date, the taxpayer gets a fresh one-year window starting January 1, 2026 to submit a refund request. There is also a two-year window to file a Voluntary Disclosure correcting errors related to that claim, provided the FTA has not yet issued a decision.

This is not a permanent extension. It is a one-time opportunity to recover old credits before they disappear permanently.

What to do: Pull your VAT records by tax period. Identify any credit balances from 2020 or 2021. Calculate when the five-year window closes. If deadlines fall in 2026, file refund applications now or use the credits to offset current liabilities.

FTA Audit Powers

The FTA's ability to audit has expanded, but within defined limits.

Under the amendments, the FTA can conduct audits or issue assessments after the standard limitation period in specific cases. The main trigger is late refund requests. If a taxpayer submits a refund claim in the final year of the five-year window, the FTA can audit that claim even after the limitation period would otherwise have closed.

The logic is straightforward. Last-minute refund claims carry higher risk of error or abuse. The FTA wants the ability to verify them properly.

For businesses, this changes the calculus on timing. Submitting a refund request close to the deadline is no longer just a procedural choice. It may invite scrutiny that an earlier claim would not have attracted.

Beyond specific triggers, FTA audit selection is risk-based. The authority uses data analytics and cross-verification to identify targets. The patterns that attract attention include discrepancies between corporate tax returns and VAT filings, revenue figures that do not reconcile across submissions, sharp profit swings without business justification, consistent losses when competitors are profitable, frequent voluntary disclosures, and large or unusual refund claims.

The FTA's systems are getting better at spotting inconsistencies. Businesses that treat corporate tax and VAT as separate compliance exercises, without reconciling them to each other, are creating exactly the kind of red flags that trigger audits.

Binding Directions

The FTA now has authority to issue official, binding directions on how specific tax provisions should be applied.

This is a structural change in how tax disputes will be resolved. Instead of taxpayers and the FTA arguing about interpretation, the FTA can issue a direction that settles the question. These directions bind both the taxpayer and the FTA itself.

The upside is consistency. Where a direction is issued, everyone applies the rule the same way.

The downside is reduced flexibility. If the FTA issues a direction that goes against your preferred interpretation, that interpretation is no longer available. You cannot argue for an alternative reading once a binding direction exists.

Businesses should monitor FTA publications. Where directions are issued on points relevant to your operations, update your compliance approach accordingly.

VAT: Self-Invoicing Goes Away

Under the reverse charge mechanism, a UAE business importing services or certain goods for business purposes must account for VAT on the supply. Previously, this required issuing a tax invoice to yourself.

From January 1, 2026, that requirement is removed. No more self-invoicing for reverse charge transactions.

This simplifies compliance, but it shifts the audit trail. Without a self-invoice as documentation, the FTA will look at supporting records instead: contracts, purchase orders, delivery confirmations, payment evidence. Businesses need to ensure these documents are complete and accessible.

VAT: Input Tax Recovery Gets Harder

The amendments give the FTA explicit power to deny input VAT recovery where a supply was connected to tax evasion and the recipient knew or should have known.

This is significant. Previously, a business could rely on the fact that VAT was charged by the supplier and paid. Under the new rules, that may not be enough.

The situations where denial risk arises:

Reverse charge should have applied. The supplier charged VAT on a supply that should have been subject to reverse charge. The supplier did not remit the VAT to the FTA. The recipient's input VAT claim may be denied because the recipient should have recognized the correct treatment.

VAT charged on exempt or out-of-scope supplies. If VAT was charged where it should not have been, and the recipient should reasonably have identified the error, recovery may be denied.

Supplier not properly registered. If VAT is charged by an entity that is not VAT-registered or not entitled to charge VAT, accepting the invoice without verification may not protect the recipient.

The test is whether the recipient "knew or should have known" about the problem. This imports a due diligence obligation. Accepting VAT invoices at face value is no longer sufficient. Businesses need to verify that the VAT treatment is correct before claiming input tax recovery.

What to do: Review your supplier verification processes. For significant transactions, confirm the supplier's VAT registration status and whether the VAT treatment on the invoice is correct. Document that verification.

VAT Credits: Five-Year Carry-Forward Limit

Excess input VAT that is not refunded can no longer be carried forward indefinitely.

From January 1, 2026, the carry-forward period is capped at five years from the end of the tax period in which the excess arose. After that, unused credits expire.

This aligns with the general five-year refund window under the Tax Procedures Law. The message is clear: use your credits or lose them.

Corporate Tax Rates Unchanged

The corporate tax structure under Federal Decree-Law No. 47 of 2022 stays the same:

- 0% on taxable income up to AED 375,000

- 9% on taxable income above AED 375,000

The AED 375,000 threshold is a tax band, not an exemption. Every business subject to corporate tax must register, file returns, and comply, even if taxable income falls within the zero-rate band.

Filing deadline: nine months from the end of the financial year. A business with a December 31, 2025 year-end must file by September 30, 2026. Payment is due by the same deadline.

Small Business Relief

Small Business Relief remains available for qualifying resident taxpayers with revenue up to AED 3 million, for tax periods ending on or before December 31, 2026.

Electing SBR treats taxable income as zero for the period. But there is a trade-off: no carry-forward of losses or net interest expense while SBR is elected.

For some businesses, preserving losses for future use is more valuable than eliminating current-year tax. The decision requires analysis, not assumption.

SBR is not available to Qualifying Free Zone Persons or members of large multinational groups.

Transfer Pricing

The UAE's transfer pricing rules align with OECD Transfer Pricing Guidelines. Documentation requirements apply to businesses with UAE revenue exceeding AED 200 million, or members of MNE groups with consolidated revenue over AED 3.15 billion.

The key requirement: transfer pricing documentation must be provided within 30 calendar days of an FTA request.

That window does not leave time to prepare documentation from scratch. Businesses with related-party transactions need contemporaneous records demonstrating arm's length pricing. Benchmarking studies, functional analyses, and intercompany agreements should be current, not created after the fact.

The FTA is paying attention to transfer pricing, particularly in free zone structures where related-party transactions can shift income between qualifying and non-qualifying activities.

Free Zone Compliance

Free zone businesses that qualify as Qualifying Free Zone Persons benefit from 0% corporate tax on qualifying income. But qualification requires more than a free zone license.

Under Cabinet Decision No. 100 of 2023, a business must demonstrate qualifying income from qualifying activities, adequate economic substance in the UAE, proper documentation, and arm's length pricing for related-party transactions.

The FTA is increasingly focused on free zone compliance. Common issues include related-party transactions priced below market, insufficient substance in the free zone, income that does not meet qualifying criteria, and poor documentation of the basis for 0% treatment.

A free zone business that claims 0% treatment but cannot support the claim during audit faces tax exposure on all non-qualifying income, penalties for incorrect filing, and potential transfer pricing adjustments.

For businesses considering DIFC or Abu Dhabi free zones, structuring for QFZP status from the outset is critical. Our international structuring team advises on entity design that meets substance requirements.

Penalties

The penalty framework for non-compliance is substantial.

Late registration: AED 10,000. A one-time waiver is available for businesses that file their first return within seven months of the end of their first tax period.

Late filing: AED 500 per month for the first 12 months, AED 1,000 per month thereafter. These penalties apply even if no tax is due.

Late payment: 14% annual interest on outstanding amounts, with no cap. The interest accrues from the day after the deadline until payment.

Voluntary disclosure vs FTA discovery: If you find an error and disclose it voluntarily, the penalty is lower. If the FTA finds the error during an audit, the penalty is 15% of the underpaid amount plus monthly interest. The difference is substantial.

A business that underpaid AED 50,000 and discloses voluntarily faces a lower penalty than one where the FTA discovers the same error. Early disclosure is cheaper than waiting to be caught.

If you are facing an FTA audit or need to file a reconsideration request, our tax disputes team represents clients through the full appeal process.

E-Invoicing

Cabinet Decision No. 106 of 2025 introduces penalties for e-invoicing non-compliance, effective from mid-2026.

For businesses required to use the Electronic Invoicing System:

- AED 5,000 per month for failure to implement the system or appoint an approved service provider by the deadline

- AED 100 per invoice or credit note not issued or transmitted on time

- AED 1,000 per day for delay in notifying the FTA of system failures

The e-invoicing mandate will roll out in phases starting with a voluntary pilot in July 2026, followed by mandatory compliance for businesses with revenue exceeding AED 50 million by January 2027. Smaller businesses follow in subsequent phases.

What To Do Before January 1, 2026

Review VAT credit balances. Identify credits by originating tax period. Calculate when each five-year window closes. File refund applications or use credits before deadlines expire.

Reconcile tax filings. Ensure corporate tax returns and VAT filings are consistent. Discrepancies trigger audits.

Assess transitional relief. For credits where the five-year period has already expired or will expire within one year of January 2026, prepare to use the one-year transitional window.

Update transfer pricing documentation. If not current, update before any FTA request.

Review input VAT practices. Implement supplier verification. Document due diligence on VAT treatment.

Evaluate Small Business Relief. If eligible, decide whether electing SBR makes sense versus preserving losses.

Key Takeaways

The 2026 changes do not raise tax rates. They tighten administration.

Credits expire after five years. Old VAT balances need attention now.

The FTA can audit late refund claims beyond the normal limitation period.

Binding directions will standardize interpretation, reducing room for argument.

Input VAT recovery requires due diligence, not just a valid invoice.

Self-invoicing for reverse charge is gone, but documentation requirements remain.

Penalties are cumulative. Voluntary disclosure costs less than audit discovery.

How Kayrouz & Associates Can Help

Kayrouz & Associates advises businesses on UAE tax compliance, structuring, and disputes.

We review credit balances and filing positions to identify risks before they become penalties. We advise on corporate tax elections, transfer pricing, and free zone structures. We represent clients in FTA audits, penalty reconsiderations, and appeals.

For businesses with ongoing compliance needs, we provide regular oversight of VAT and corporate tax filings, ensuring deadlines are met and documentation is audit-ready.

Contact our team to discuss your position.

Your success starts with the right guidance.

Whether it’s business or personal, our team provides the insight and guidance you need to succeed.